What is long term care?

Long term care is the medical and social services term for helping people who develop disabilities or chronic care needs. Services may be brief with full recovery, or they can continue for years. Most long term care is by definition custodial care which is nonmedical assistance with activities of daily living such as walking, bathing, dressing, eating or using the toilet.

Care may be required due to physical impairment or cognitive impairment. The effects of Alzheimer’s, strokes, diabetes, auto accidents, sporting accidents and dementia commonly trigger the need for long term care services.

Long term care can be received at home, in an assisted living facility or skilled nursing facility.

Who needs long term care?

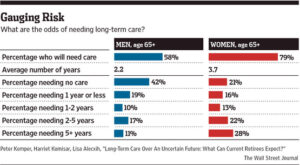

As we age, it becomes more likely we will need long term care services. The U.S. Department of Health and Human Services reports that 70% of people turning age 65 can expect to use some form of long term care during their lives. The risk is also significant for working age adults as 42% of the 13 million people receiving long term care services are between the ages of 18 and 64.

How long will you need care?

By gender, women need care for 3.7 years while men average 2.2 years of long term care. Consider that one-third of today’s 65 year olds may never need long term care services, but 20 percent will need it for longer than 5 years.

Your Options to Pay for Long Term Care

Rely on the Government?

Medicare

The national health insurance program for people over age 65 only pays for skilled, short-term care limited to 100 days. It does not cover custodial care.

Medicaid

A joint federal and state government program to help people with low income and assets. It primarily provides for institutional care in Skilled Nursing Homes after assets have been exhausted.

Spend Personal Assets?

- $306,600 risk 2019 ($102,200 annual cost of care in 2019 x 3 years of care)

- $412,044 risk 2029 ($137,348 projected annual cost in 2029 x 3 years of care)

- $553,755 risk 2039 ($184,585 projected annual cost in 2039 x 3 years of care)

Use Long Term Care Insurance to Transfer the Risk?

Long-term care insurance is designed to pay for long term services and support, including personal and custodial care in a variety of settings such as your home, assisted living facility, adult day care facility or skilled nursing facility.

Long Term Care Insurance

A long term care insurance policy reimburses you for assistance required with activities of daily living (such as walking, bathing, dressing, continence, toileting and eating), or directional reminding assistance required due to cognitive impairment from Alzheimer’s or dementia. You can select where you want to receive services and the maximum value of your long term care protection.

The cost of your long term care policy is based on:

- Your age when you buy the protection

- The maximum amount the policy will pay per day

- The maximum number of days (years) the policy will pay for care

- The lifetime maximum a policy will pay is the maximum amount per day times the maximum number of days

- Good health and spousal discounts can lower premiums significantly. Other plan design options can also lower premiums.

If you have health issues you may not qualify to purchase long term care protection because most policies require medical underwriting. Poor health may limit the amount of coverage you can purchase or you may only be able to purchase a policy at a non-standard rate.

Hybrid Long-Term Care Insurance

Hybrid long-term care plans are a variation on traditional long-term care (LTC) insurance and fall under two categories:

1) Life Insurance with a Long-Term Care Benefit

2) Annuities with a Long-Term Care Benefit

Long-term care hybrid products are also called linked benefit or asset based long-term care policies. These LTC hybrid products can offer several advantages:1

Guaranteed Benefits - They guarantee benefits will always be paid, in one form or another.

Guaranteed Premiums - Most policies guarantee that premiums will never change.

1035 Exchanges - Some asset based long-term care insurers permit 1035 exchanges. The tax advantage of utilizing a 1035 exchange is to defer the internal build up of gains associated with your existing annuity or cash value life insurance policy. 2

Long-Term Care Life Insurance

A life insurance policy with long-term care benefits works by accelerating the life insurance death benefit to pay for your long-term care. If you never need long-term care, your estate receives a tax-free death benefit.

- Depending on the policy, you can choose to pay one lump-sum premium, pay it up in 5 or 10 years, and some policies offer continuous pay premiums.

- The policy provides a pool of money for long-term care that’s equal to several times your premium payment. Some policies offer an unlimited pool of money.

- If you use your policy for long-term care, the death benefit is decreased by the amount of long-term care benefits used.

- Requires health underwriting

Long-Term Care Annuity

A long-term care annuity functions like a fixed annuity, but it has a long-term care multiplier built into the policy. If you need long-term care, a part of the contract pays the long-term care benefit.

Long-term care benefits are calculated on the amount of coverage selected when the policy is purchased. For example, the insurance company offers an LTC payout of 200% or 300% of the total policy value. A policyholder with a $100,000 annuity who had selected a total benefit limit of 300% would have an extra $200,000 available for long-term care expenses, after the initial $100,000 policy value is used. If long-term care is never needed, the annuity value is paid to the beneficiary.

- A long-term care annuity may allow you to access cash value during your lifetime -- even if you never need care.

- When the annuity contract matures, your contract’s remaining cash value may be passed on to your beneficiaries.

- Health qualification (health underwriting) is often less stringent than long-term-care life insurance and traditional long-term care insurance. This can make the long-term care annuity a valuable option if you have a pre-existing health condition, or if you've been turned down for long-term care insurance.

1The scenarios above are basic examples of how hybrid long-term care insurance works. Policies available will vary by state and coverage may differ depending on age, health, gender, premiums and benefits requested. For an accurate proposal, please contact us for an illustration specific to your situation.

2We do not offer tax or legal advice and strongly advise that you consult with your accountant or tax professional.

Long Term Care Insurance Tax Deduction

Tax-Qualified Long Term Care Insurance

Tax Deductible Premiums

Current tax laws allow for the deduction of either the actual premium or the eligible premium paid on a tax-qualified long-term care insurance policy.

- Actual premium is the actual amount of premium paid

- Eligible premium is an amount determined annually by the federal government based on the medical care components of the Consumer Price Index and the age of the policyholder

Tax-Free Benefits

The benefits paid by a tax-qualified long-term care insurance policy are intended to be tax free as long as they do not exceed the greater of:

- Qualified long-term care daily expenses, or

- The per-day limitation, which is $400 in 2023

Source: Section 7702B of the Internal Revenue Code (IRC)

Deductible Out-of-Pocket Expenses

Generally, any long-term care expense paid out-of-pocket may be claimed as a medical deduction on a federal income tax return. The only exception is payment for home care provided by a family member who is not a licensed health-care professional.

State Tax Deductions

Currently a number of states offer tax deductions and/or credits for people who purchase tax-qualified long-term care policies. These state deductions and credits are in addition to those offered by the federal government.

| Eligible Premium Guidelines for 2023 | |

| At age: | You can deduct: |

| 40 and younger | $480 |

| 41-50 | $890 |

| 51-60 | $1,790 |

| 61-70 | $4,770 |

| 71 and older | $ 5,960 |

IRS Revenue Procedure 2023-45

Tax Advantages for Individuals and Businesses

| For Individuals |

Eligible premium may be claimed as a medical expense in 2023 as long as: • Combined medical expenses exceed 7.5 percent* of adjusted gross income, and • Deductions are itemized on the federal income tax return *Percentage may be subject to change. |

|

For Self-Employed Business Owners Sole Proprietor | Partnership | LLC | S Corporation |

Eligible premium may be tax deductible when the business purchases long-term care insurance policies for: • Owner • Spouse • Dependents Actual premium may be tax deductible when the business purchases long-term care insurance policies for: • Employees |

| For Owners of C Corporations |

Actual premium may be tax deductible when the business purchases long-term care insurance policies for: • Owner/Employee* • Spouse • Dependents • Employees *The officers and owners of C Corporations may be employees, which means premium paid by the corporation for tax-qualified LTCi (QLTC) policies may be deductible by the corporation and not taxable to the employees if the contributions are made pursuant to an employee benefit plan. If the QLTC employee benefit plan is insured, it need not conform to non- discrimination rules and may be available only to a select class of employees (IRC Section 106). The corporation must be able to show that the plan covers owner- employees as employees and not as owners. QLTC coverage may not use salary reduction dollars to pay its premium contribution. If premiums are paid in advance, such as in a short-pay situation, the amount and timing of the deduction currently is unclear. The client should consult a tax advisor. |

We do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. We encourage you to consult your own tax, legal and accounting advisors.